Q1 2026 Shatters All Venture Capital Records: $300B Invested as AI Claims 80% of Global Funding

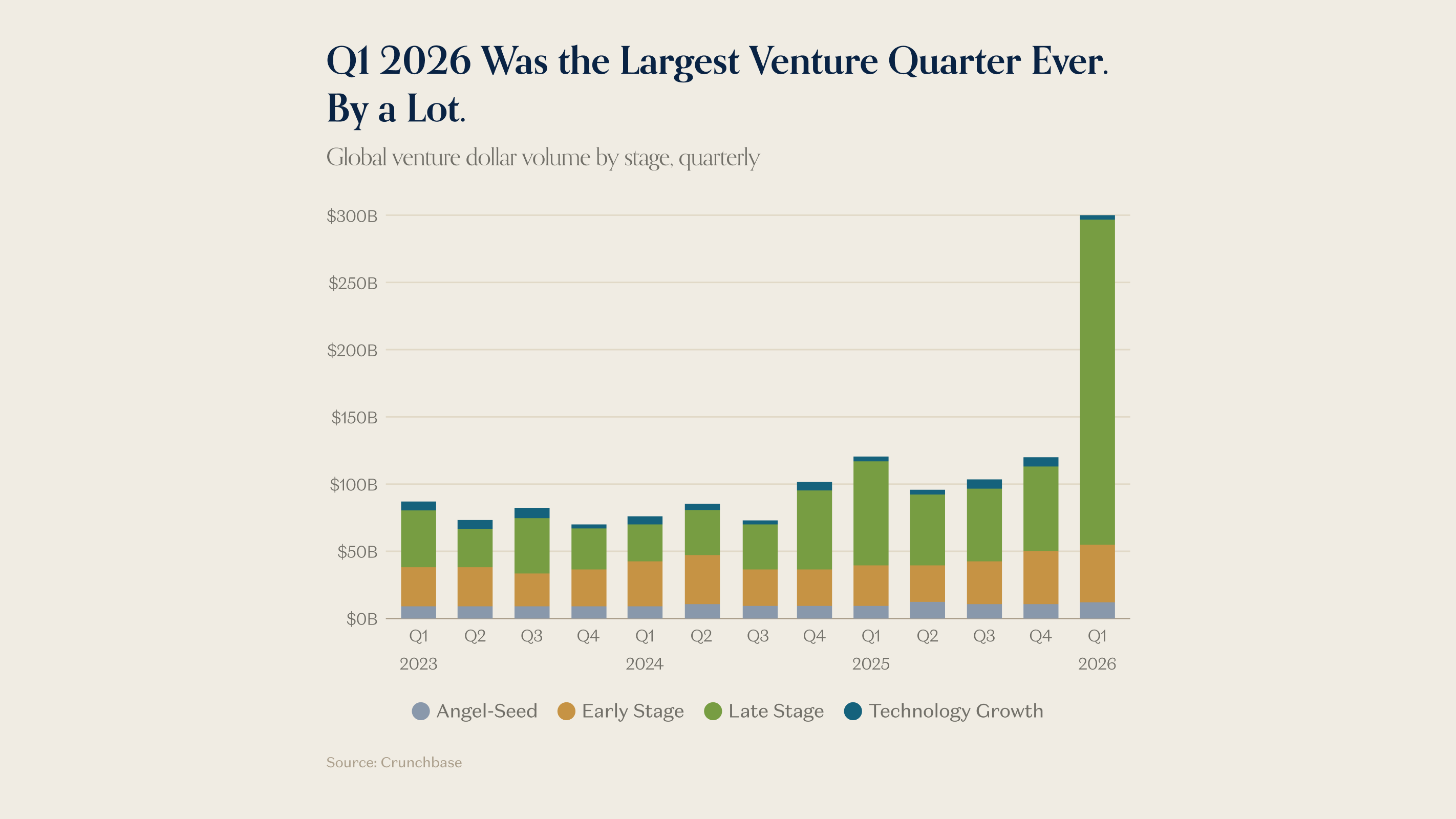

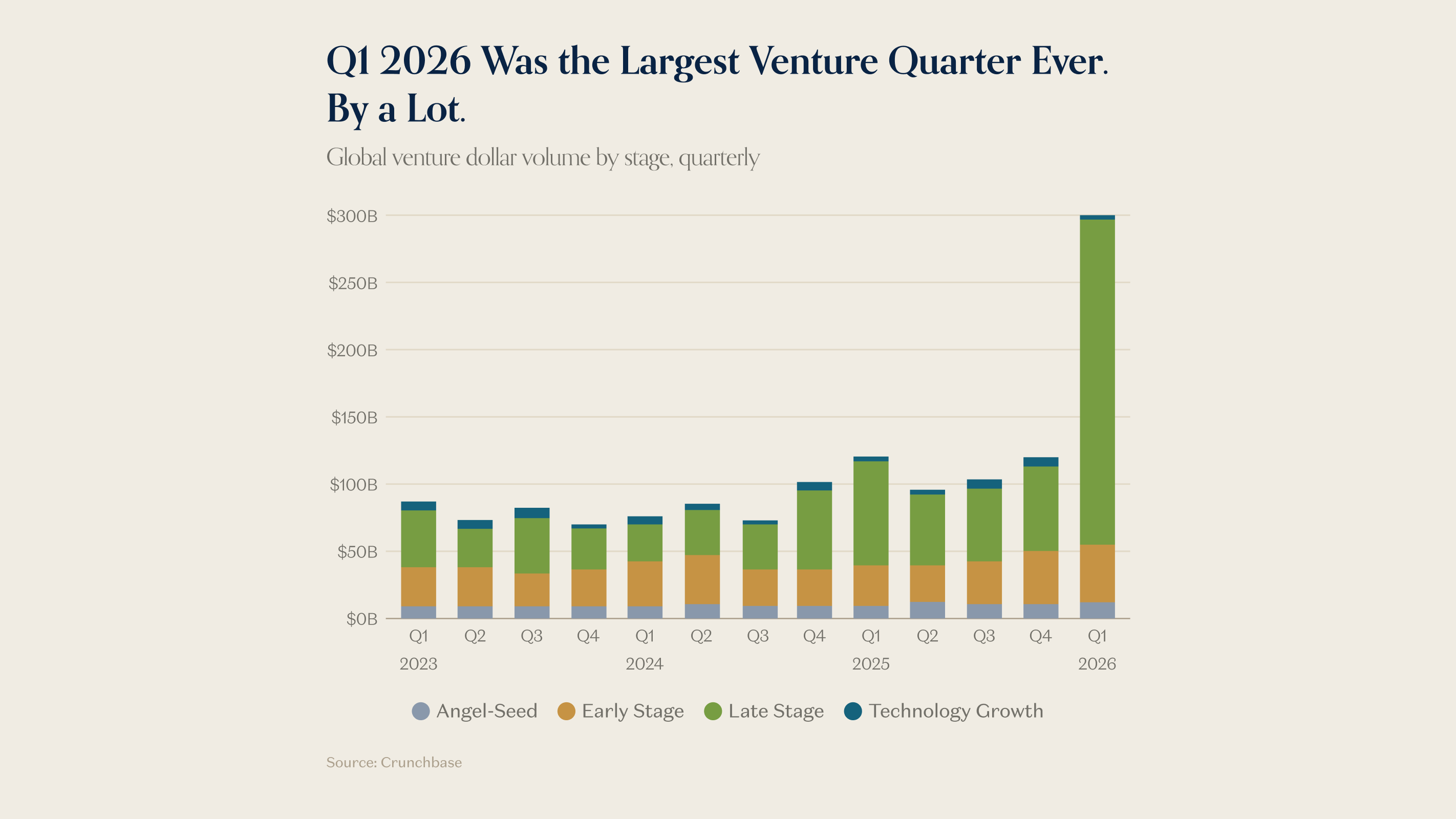

Global venture investment hit $300 billion in Q1 2026 — up 150% year-over-year and the largest single quarter in history — with AI capturing 80% of all capital. OpenAI ($122B), Anthropic ($30B), xAI ($20B), and Waymo ($16B) alone accounted for 65% of total global VC spending.

Global venture capital investment reached $300 billion across roughly 6,000 startups in — up more than 150% year-over-year and the highest single quarter on record by a wide margin. The total exceeds approximately 70% of all venture capital deployed in all of 2025, driven almost entirely by AI mega-rounds at frontier labs.

What Happened

Four companies defined the quarter. OpenAI closed a $122 billion round at a post-money valuation of $852 billion on — the largest single venture round ever recorded, backed by Amazon ($50B), Nvidia ($30B), and SoftBank ($30B), with an additional $3 billion raised from retail investors through bank channels. Anthropic raised $30 billion, xAI secured $20 billion, and autonomous driving company Waymo closed a $16 billion round. Combined, these four deals total $188 billion — roughly 65% of all global venture capital in the quarter.

According to Crunchbase data published , AI received approximately $242 billion, or 80% of total funding — up sharply from 55% in Q1 2025. Late-stage investment totaled $246.6 billion across 584 deals, a 205% increase year-over-year. Early-stage funding rose 41% in dollar terms to $41.3 billion, though seed deal count fell 30%, indicating a trend toward fewer, larger bets.

Key Details

- $300B total — all-time quarterly record, up 150%+ year-over-year and quarter-over-quarter

- AI captured $242B (80%) — up from 55% in Q1 2025; previous annual record was 55%

- US dominated with $250B (83%) — China second at $16.1B, UK third at $7.4B

- OpenAI valued at $852B — $122B round is largest single venture round in history; generating $2B/month in revenue

- 21 unicorn exits above $1B — M&A volume totaled $56.6B; IPO market remained slow in the US

- Seed deal count fell 30% despite seed dollars rising 31% — concentration of capital is compressing the early-stage market

- Unicorn portfolio gained $900B in valuation — in a single quarter, reflecting AI-driven repricing across the market

What Developers and Investors Are Saying

Reaction across Hacker News, Reddit, and VC Twitter has been a mix of awe and concern. The dominant narrative from investors: this is not a bubble in the traditional sense — the underlying revenue at frontier labs (OpenAI at $2B/month, growing fast) justifies at least some of the valuation expansion. But the concentration of capital is alarming to many founders outside AI. As a16z noted in their quarterly analysis: "When 80% of all global venture capital flows to one sector in a quarter, founders building outside it aren't competing on a level field — they are competing in a secondary capital tier." On Reddit's r/startups, the top threads debate whether this marks the peak of the AI investment cycle or the beginning of sustained infrastructure spending akin to the cloud build-out of the 2010s. Several seed-stage founders noted that LP attention is almost entirely consumed by frontier lab opportunities, making it harder to raise rounds even at strong traction metrics.

What This Means for Developers

For developers, the immediate practical implication is a continued flood of well-funded AI infrastructure. More compute, cheaper APIs, and more aggressive tooling from companies flush with capital. OpenAI's $122B raise is specifically earmarked to accelerate compute buildout — which should translate to lower inference costs and faster model iteration over the next 12–18 months. The Waymo and broader robotics/autonomous systems investment suggests a parallel buildout in physical AI infrastructure. For developers building outside AI — in SaaS, dev tools, or consumer apps — fundraising conditions remain difficult. The secondary capital tier is real: seed investors are consolidating around a smaller number of AI-adjacent bets, and traditional SaaS multiples are contracting. Teams should plan for longer paths to funding and lean further on bootstrapping and revenue-based growth strategies in 2026.

What's Next

All eyes are on the IPO market. OpenAI has signaled an IPO path, and at $852B valuation it would be one of the largest public listings in history. Analysts expect Q2 2026 to show normalization from Q1's extraordinary mega-rounds, but the underlying AI infrastructure spending cycle is expected to continue through at least 2027. Watch for secondary market activity as employees at OpenAI, Anthropic, and xAI gain liquidity. The NVDA/SoftBank anchor stakes in OpenAI also signal a deepening of the semiconductor-to-model company vertical integration that could reshape how the entire AI stack is owned and monetized.

Sources

- Crunchbase News — Primary VC data source for Q1 2026 global funding figures

- a16z Charts of the Week — Analysis and charts on AI funding concentration

- OpenAI Official Blog — Announcement of $122B funding round

- TechRound — Independent coverage of the Q1 2026 VC record

- Foley & Lardner — Legal and market analysis of Q1 2026 conditions

- Evermx — Breakdown of AI share and deal concentration data

Stay up to date with Doolpa

Subscribe to Newsletter →